6. Indexgestützte Aktienauswahlstrategie

Referenzquelle: docs/_joinquant_migration_source/Example_06_index-enhanced stock selection.ipynb Erste Markdown-Zelle.

Diese Strategie bildet die im CSI 300 enthaltenen Aktien mit einer Gewichtung von über 0,35 % anhand einer anfänglichen Gewichtung von 0,8 ab. Der prozentuale Anteil jeder einzelnen Aktie wird wie folgt berechnet: (0,8 * Gewichtung der enthaltenen Aktie) * 100 %. Anschließend wird, je nachdem, ob eine Aktie 1. fünf Tage in Folge gestiegen oder 2. fünf Tage in Folge gefallen ist, entschieden, ob es sich um eine starke oder schwache Aktie handelt. Ihre Gewichtung wird entsprechend von 0,8 auf 1,0 oder 0,6 angepasst.

Häufigkeit der Strategieausführung: Täglich; Zeitpunkt der Strategieausführung: Vor Börsenschluss jeden Tag.

Der Backtesting-Zeitraum erstreckte sich vom 1. Januar 2021 bis zum 31. Dezember 2022.

6.1. 1. 策略代码

Erstellen Sie individuelle Handelsstrategien:

import qteasy as qt

import numpy as np

from qteasy import Parameter, StgData

class IndexEnhancement(qt.GeneralStg):

def __init__(self):

super().__init__(

pars=[

Parameter((0.01, 0.99), name='weight_threshold', par_type='float', value=0.35),

Parameter((0.51, 0.99), name='init_weight', par_type='float', value=0.8),

Parameter((2, 20), name='price_days', par_type='int', value=5),

],

name='IndexEnhancement',

description='跟踪HS300指数选股,并根据连续上涨/下跌趋势判断强弱势以增强权重',

data_types=[

StgData('wt_idx|000300.SH', freq='m', asset_type='E', window_length=2),

StgData('close', freq='d', asset_type='E', window_length=40),

],

)

def realize(self):

weight_threshold, init_weight, price_days = self.get_pars('weight_threshold', 'init_weight', 'price_days')

# 读取投资组合的权重wt和最近price_days天的收盘价

wt = self.get_data('wt_idx|000300.SH_E_m')[-1]

close_windows = self.get_data('close_E_d')

pre_close = close_windows[-price_days - 1:-1]

close = close_windows[-price_days:] # 当前所有股票的最新连续收盘价

# 计算连续price_days天的收益

stock_returns = close - pre_close

# 设置初始选股权重为0.8

weights = init_weight * np.ones_like(wt)

# 剔除掉权重小于weight_threshold的股票

weights[wt < weight_threshold] = 0

# 找出强势股,将其权重设为1, 找出弱势股,将其权重设置为 init_weight - (1 - init_weight)

up_trends = np.all(stock_returns > 0, axis=1)

weights[up_trends] = 1.0

down_trend_weight = init_weight - (1 - init_weight)

down_trends = np.all(stock_returns < 0, axis=1)

weights[down_trends] = down_trend_weight

# 实际选股权重为weights * HS300权重

weights *= wt

return weights

6.2. 2. 策略回测

Backtesting-Parameter:

Backtesting-Zeitraum: 1. Januar 2021 bis 31. Dezember 2022

Anlageart: Aktien

Vermögenspool: Aktien des CSI 300

Anfangskapital: 1 Million

Kaufmenge: 100 Aktien

Verkaufsmenge: 1 Stück

shares = qt.filter_stock_codes(index='000300.SH', date='20210101')

print(len(shares), shares[:10])

alpha = IndexEnhancement()

op = qt.Operator(alpha, signal_type='PT')

op.op_type = 'stepwise'

op.set_blender('1.0*s0')

res = qt.run(op, mode=1,

invest_start='20210101',

invest_end='20221231',

invest_cash_amounts=[1000000],

asset_type='E',

asset_pool=shares,

trade_batch_size=100,

sell_batch_size=1,

trade_log=True,

)

print()

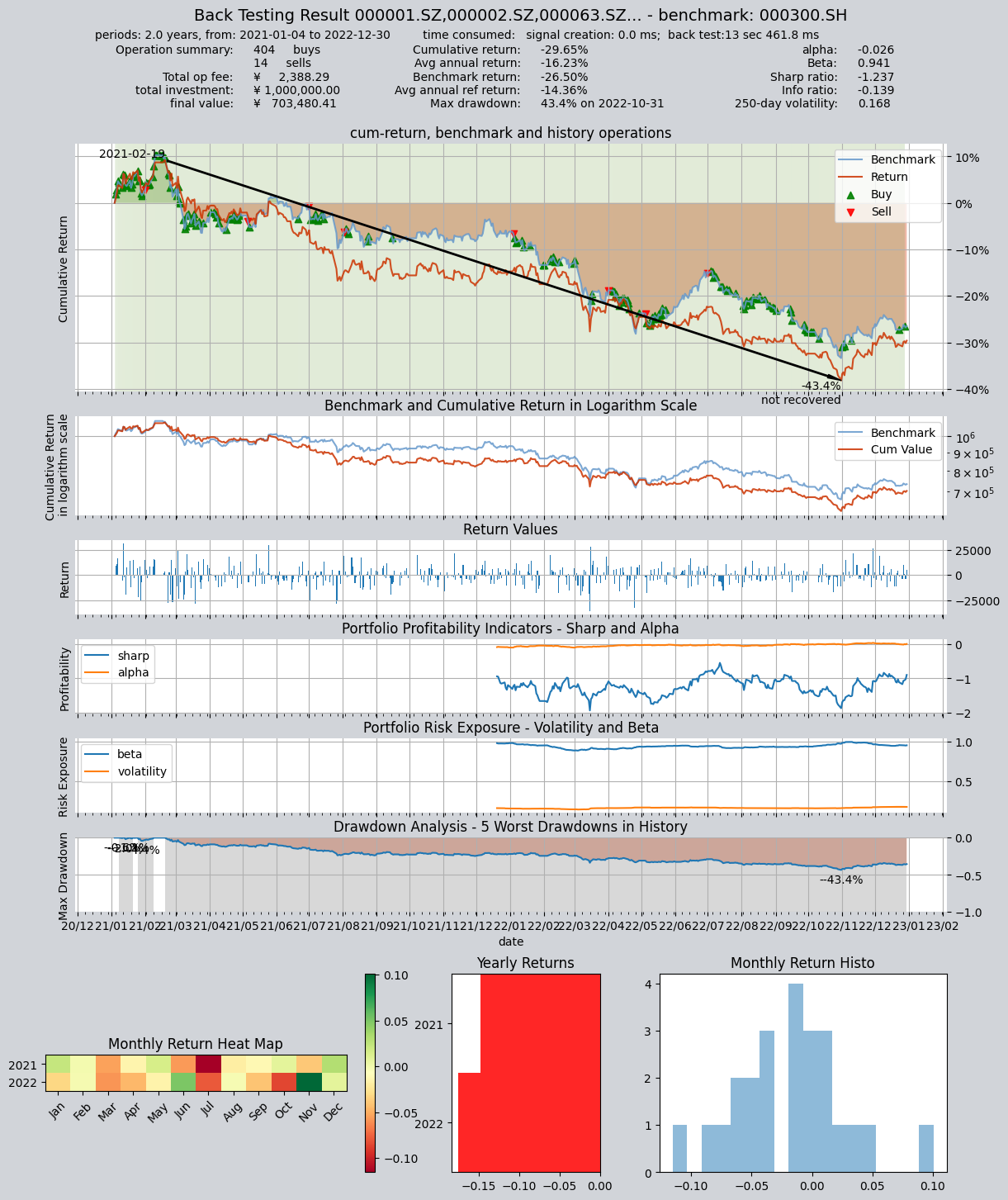

6.3. Backtesting-Ergebnisse

419 ['000001.SZ', '000002.SZ', '000063.SZ', '000066.SZ', '000069.SZ', '000100.SZ', '000157.SZ', '000166.SZ', '000333.SZ', '000338.SZ']

No match found! To get better result, you can

- pass "match_full_name=True" to match full names of stocks and funds

====================================

| |

| BACK TESTING RESULT |

| |

====================================

qteasy running mode: 1 - History back testing

time consumption for operate signal creation: 0.0 ms

time consumption for operation back looping: 13 sec 461.8 ms

investment starts on 2021-01-04 00:00:00

ends on 2022-12-30 00:00:00

Total looped periods: 2.0 years.

-------------operation summary:------------

Only non-empty shares are displayed, call

"loop_result["oper_count"]" for complete operation summary

Sell Cnt Buy Cnt Total Long pct Short pct Empty pct

000001.SZ 0 3 3 100.0% 0.0% 0.0%

000002.SZ 0 2 2 100.0% 0.0% 0.0%

000063.SZ 0 0 0 100.0% 0.0% 0.0%

000100.SZ 1 5 6 66.9% 0.0% 33.1%

000333.SZ 0 1 1 100.0% 0.0% 0.0%

000338.SZ 1 1 2 62.3% 0.0% 37.7%

000651.SZ 0 1 1 100.0% 0.0% 0.0%

000725.SZ 0 95 95 100.0% 0.0% 0.0%

000858.SZ 0 0 0 100.0% 0.0% 0.0%

002027.SZ 1 3 4 62.3% 0.0% 37.7%

... ... ... ... ... ... ...

601229.SH 1 3 4 50.2% 0.0% 49.8%

601288.SH 0 76 76 100.0% 0.0% 0.0%

601318.SH 0 3 3 100.0% 0.0% 0.0%

601328.SH 0 30 30 100.0% 0.0% 0.0%

601398.SH 0 106 106 100.0% 0.0% 0.0%

601601.SH 1 0 1 78.8% 0.0% 21.2%

601668.SH 0 15 15 100.0% 0.0% 0.0%

601688.SH 0 1 1 100.0% 0.0% 0.0%

601899.SH 0 4 4 100.0% 0.0% 0.0%

603259.SH 0 0 0 100.0% 0.0% 0.0%

Total operation fee: ¥ 2,388.29

total investment amount: ¥1,000,000.00

final value: ¥ 703,480.41

Total return: -29.65%

Avg Yearly return: -16.23%

Skewness: -0.02

Kurtosis: 1.63

Benchmark return: -26.50%

Benchmark Yearly return: -14.36%

------strategy loop_results indicators------

alpha: -0.026

Beta: 0.941

Sharp ratio: -1.237

Info ratio: -0.139

250 day volatility: 0.168

Max drawdown: 43.41%

peak / valley: 2021-02-19 / 2022-10-31

recovered on: Not recovered!

===========END OF REPORT=============