5. Psuedo-Grid Trading Strategy

Reference source: docs/_joinquant_migration_source/Example_05_Class Grid Trading.ipynb First Markdown cell.

This strategy first calculates the mean and standard deviation of the past 300 price data points (the number of days is an adjustable parameter).

The grid interval boundaries are obtained by adding or subtracting 1 and 2 standard deviations from the mean (the multiplier for adding or subtracting standard deviations is an adjustable parameter).

They are assigned position weights of 0.3 and 0.5 respectively (position weights are adjustable parameters).

Then, configure the position size based on the price range (+/-40 is the upper and lower bound, which has no practical significance): (-40,-3],(-3,-2],(-2,2],(2,3],(3,40] (the specific price is equal to the mean plus a multiple of the standard deviation) [-0.5, -0.3, 0.0, 0.3, 0.5] (capital ratio; the negative sign here indicates opening a short position, and it is set to allow holding short positions during backtesting).

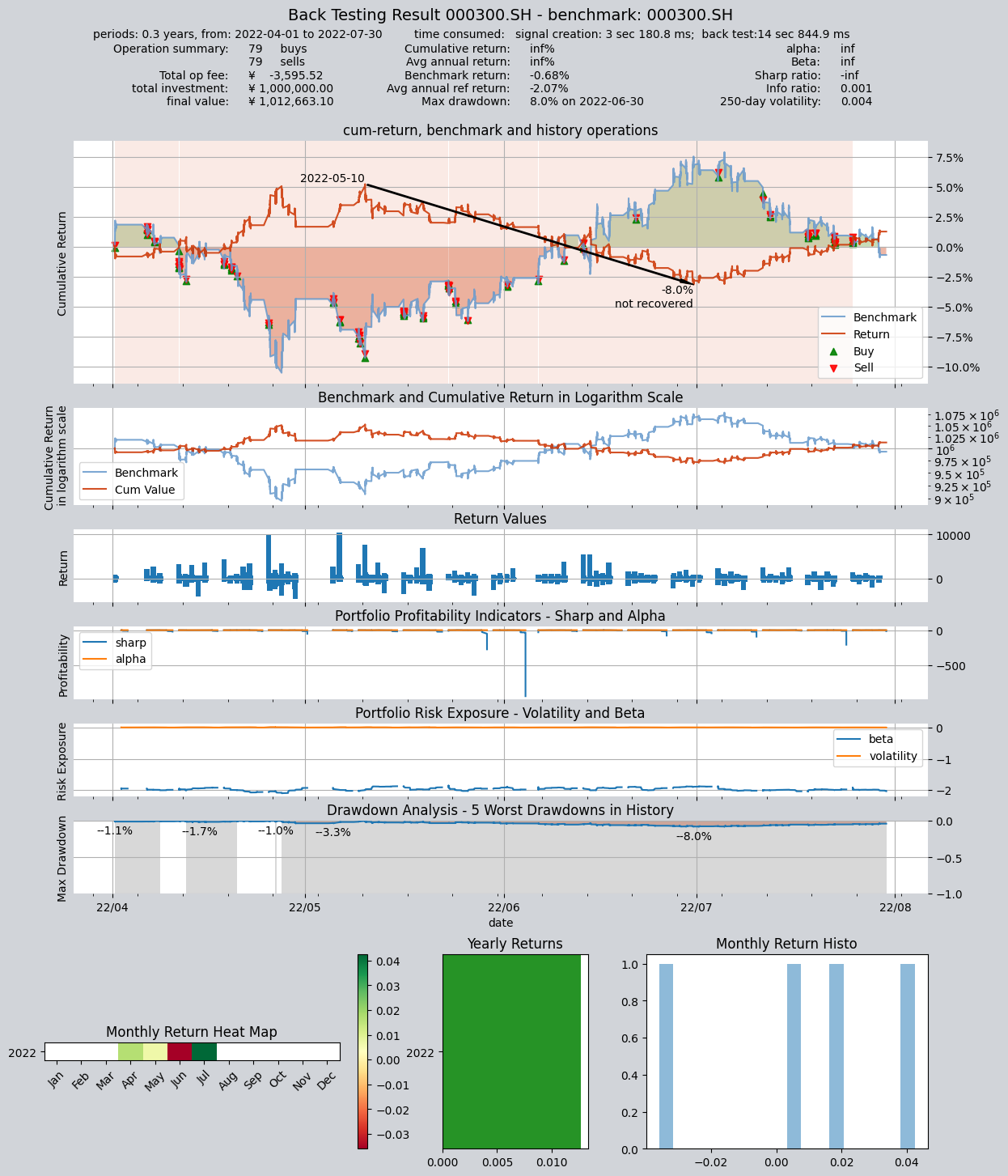

The backtesting data consists of 1-minute data points for the HS300 index. The backtesting period is from 09:30:00 on March 1, 2022 to 15:00:00 on July 31, 2022.

import qteasy as qt

print(qt.__version__)

5.1. Define trading strategy

import numpy as np

from qteasy import Parameter, StgData

class GridTrading(qt.GeneralStg):

def __init__(self):

super().__init__(

name='GridTrading',

description='根据过去窗口的均值和标准差分档生成目标仓位',

pars=[

Parameter((0.5, 3.0), name='low_th', par_type='float', value=2.0),

Parameter((2.0, 8.0), name='high_th', par_type='float', value=3.0),

Parameter((0.01, 0.6), name='low_pos', par_type='float', value=0.3),

Parameter((0.1, 1.0), name='high_pos', par_type='float', value=0.5),

Parameter((60, 500), name='lookback', par_type='int', value=300),

],

data_types=StgData('close', freq='1min', asset_type='ANY', window_length=500),

use_latest_data_cycle=False,

)

def realize(self):

low_th, high_th, low_pos, high_pos, lookback = self.get_pars(

'low_th', 'high_th', 'low_pos', 'high_pos', 'lookback'

)

close = self.get_data('close_ANY_1min')

close = close[-lookback:]

close_mean = np.nanmean(close, axis=0)

close_std = np.nanstd(close, axis=0)

current_close = close[-1]

hi_positive = close_mean + high_th * close_std

low_positive = close_mean + low_th * close_std

low_negative = close_mean - low_th * close_std

hi_negative = close_mean - high_th * close_std

pos = np.zeros_like(close_mean, dtype=float)

pos = np.where(current_close > hi_positive, high_pos, pos)

pos = np.where((current_close <= hi_positive) & (current_close > low_positive), low_pos, pos)

pos = np.where((current_close <= low_positive) & (current_close > low_negative), 0.0, pos)

pos = np.where((current_close <= low_negative) & (current_close > hi_negative), -low_pos, pos)

pos = np.where(current_close <= hi_negative, -high_pos, pos)

return pos

5.2. Define the trader object, configure the trading settings, and perform trading backtesting.

alpha = GridTrading()

op = qt.Operator(alpha, signal_type='PT')

op.op_type = 'batch'

op.set_blender("1.0*s0")

res = qt.run(op,

mode=1,

invest_start='20220401',

invest_end='20220731',

invest_cash_amounts=[1000000],

asset_type='IDX',

asset_pool=['000300.SH'],

trade_batch_size=0.01,

sell_batch_size=0.01,

trade_log=True,

allow_sell_short=True,

)

====================================

| |

| BACK TESTING RESULT |

| |

====================================

qteasy running mode: 1 - History back testing

time consumption for operate signal creation: 3 sec 180.8 ms

time consumption for operation back looping: 14 sec 844.9 ms

investment starts on 2022-04-01 09:30:00

ends on 2022-07-30 15:00:00

Total looped periods: 0.3 years.

-------------operation summary:------------

Only non-empty shares are displayed, call

"loop_result["oper_count"]" for complete operation summary

Sell Cnt Buy Cnt Total Long pct Short pct Empty pct

000300.SH 79 79 158 0.0% 98.1% 1.9%

Total operation fee: ¥ -3,595.52

total investment amount: ¥1,000,000.00

final value: ¥1,012,663.10

Total return: inf%

Avg Yearly return: inf%

Skewness: 3.34

Kurtosis: 116.90

Benchmark return: -0.68%

Benchmark Yearly return: -2.07%

------strategy loop_results indicators------

alpha: inf

Beta: inf

Sharp ratio: -inf

Info ratio: 0.001

250 day volatility: 0.004

Max drawdown: 7.95%

peak / valley: 2022-05-10 / 2022-06-30

recovered on: Not recovered!

===========END OF REPORT=============