5. Estrategia comercial pseudo-grid

Fuente de referencia: docs/_joinquant_migration_source/Example_05_Class Grid Trading.ipynb Primera celda de Markdown.

Esta estrategia primero calcula la media y la desviación estándar de los últimos 300 puntos de datos de precios (el número de días es un parámetro ajustable).

Los límites del intervalo de la cuadrícula se obtienen sumando o restando 1 y 2 desviaciones estándar de la media (el multiplicador para sumar o restar desviaciones estándar es un parámetro ajustable).

Se les asignan pesos de posición de 0,3 y 0,5 respectivamente (los pesos de posición son parámetros ajustables).

Luego, configure el tamaño de la posición según el rango de precios (+/-40 es el límite superior e inferior, lo cual no tiene significado práctico): (-40,-3],(-3,-2],(-2,2],(2,3],(3,40] (el precio específico es igual a la media más un múltiplo de la desviación estándar) [-0.5, -0.3, 0.0, 0.3, 0.5] (ratio de capital; el signo negativo aquí indica abrir una posición corta y está configurado para permitir mantener posiciones cortas durante el backtesting).

Los datos del backtesting constan de puntos de datos de 1 minuto para el índice HS300. El periodo de backtesting es desde las 09:30:00 horas del 1 de marzo de 2022 hasta las 15:00:00 horas del 31 de julio de 2022.

import qteasy as qt

print(qt.__version__)

5.1. Definir la estrategia comercial

import numpy as np

from qteasy import Parameter, StgData

class GridTrading(qt.GeneralStg):

def __init__(self):

super().__init__(

name='GridTrading',

description='根据过去窗口的均值和标准差分档生成目标仓位',

pars=[

Parameter((0.5, 3.0), name='low_th', par_type='float', value=2.0),

Parameter((2.0, 8.0), name='high_th', par_type='float', value=3.0),

Parameter((0.01, 0.6), name='low_pos', par_type='float', value=0.3),

Parameter((0.1, 1.0), name='high_pos', par_type='float', value=0.5),

Parameter((60, 500), name='lookback', par_type='int', value=300),

],

data_types=StgData('close', freq='1min', asset_type='ANY', window_length=500),

use_latest_data_cycle=False,

)

def realize(self):

low_th, high_th, low_pos, high_pos, lookback = self.get_pars(

'low_th', 'high_th', 'low_pos', 'high_pos', 'lookback'

)

close = self.get_data('close_ANY_1min')

close = close[-lookback:]

close_mean = np.nanmean(close, axis=0)

close_std = np.nanstd(close, axis=0)

current_close = close[-1]

hi_positive = close_mean + high_th * close_std

low_positive = close_mean + low_th * close_std

low_negative = close_mean - low_th * close_std

hi_negative = close_mean - high_th * close_std

pos = np.zeros_like(close_mean, dtype=float)

pos = np.where(current_close > hi_positive, high_pos, pos)

pos = np.where((current_close <= hi_positive) & (current_close > low_positive), low_pos, pos)

pos = np.where((current_close <= low_positive) & (current_close > low_negative), 0.0, pos)

pos = np.where((current_close <= low_negative) & (current_close > hi_negative), -low_pos, pos)

pos = np.where(current_close <= hi_negative, -high_pos, pos)

return pos

5.2. Defina el objeto comercial, configure los ajustes comerciales y realice pruebas retrospectivas comerciales.

alpha = GridTrading()

op = qt.Operator(alpha, signal_type='PT')

op.op_type = 'batch'

op.set_blender("1.0*s0")

res = qt.run(op,

mode=1,

invest_start='20220401',

invest_end='20220731',

invest_cash_amounts=[1000000],

asset_type='IDX',

asset_pool=['000300.SH'],

trade_batch_size=0.01,

sell_batch_size=0.01,

trade_log=True,

allow_sell_short=True,

)

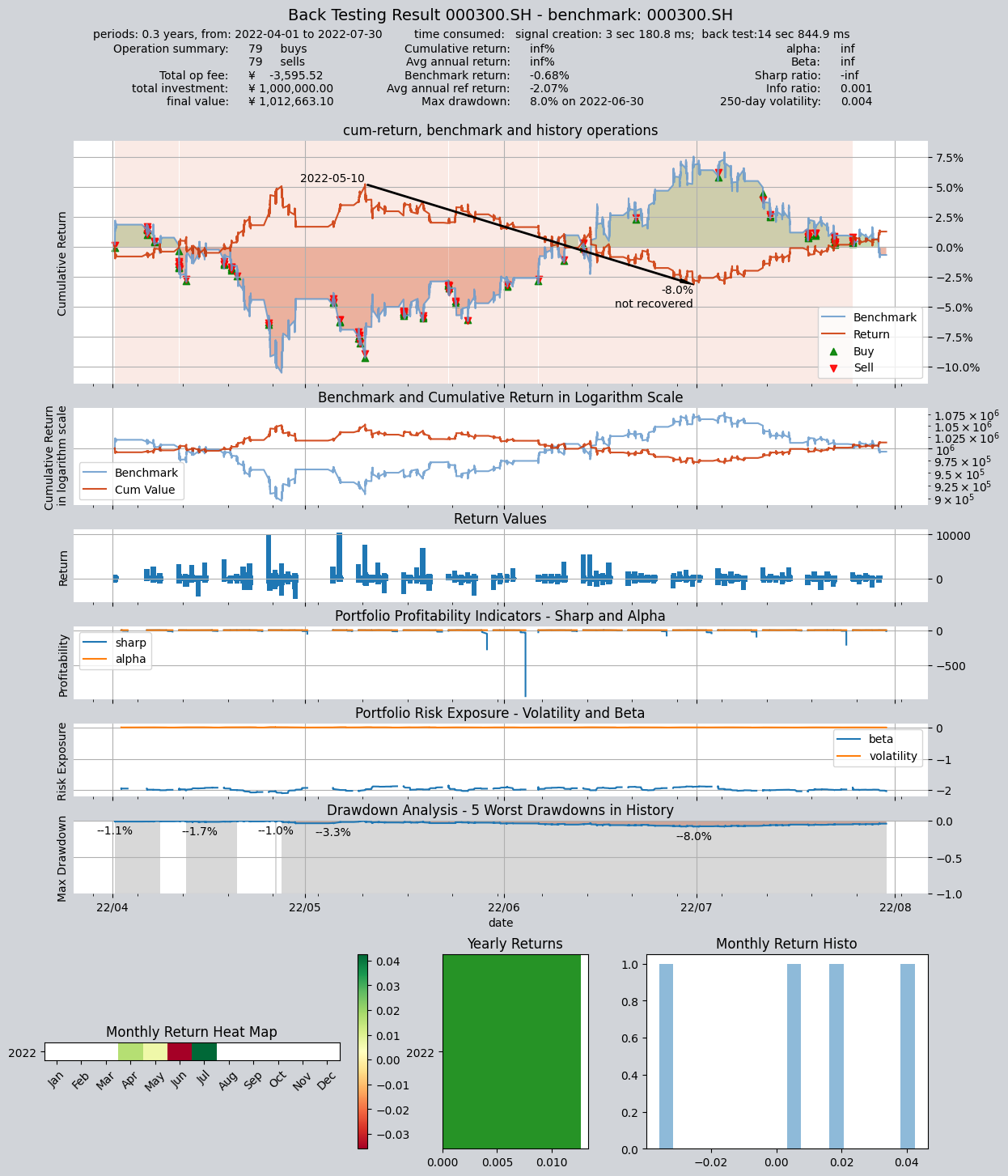

====================================

| |

| BACK TESTING RESULT |

| |

====================================

qteasy running mode: 1 - History back testing

time consumption for operate signal creation: 3 sec 180.8 ms

time consumption for operation back looping: 14 sec 844.9 ms

investment starts on 2022-04-01 09:30:00

ends on 2022-07-30 15:00:00

Total looped periods: 0.3 years.

-------------operation summary:------------

Only non-empty shares are displayed, call

"loop_result["oper_count"]" for complete operation summary

Sell Cnt Buy Cnt Total Long pct Short pct Empty pct

000300.SH 79 79 158 0.0% 98.1% 1.9%

Total operation fee: ¥ -3,595.52

total investment amount: ¥1,000,000.00

final value: ¥1,012,663.10

Total return: inf%

Avg Yearly return: inf%

Skewness: 3.34

Kurtosis: 116.90

Benchmark return: -0.68%

Benchmark Yearly return: -2.07%

------strategy loop_results indicators------

alpha: inf

Beta: inf

Sharp ratio: -inf

Info ratio: 0.001

250 day volatility: 0.004

Max drawdown: 7.95%

peak / valley: 2022-05-10 / 2022-06-30

recovered on: Not recovered!

===========END OF REPORT=============